|

Need more info or you couldn't find what you were looking for, let us know by sending an email to: support@dancik.com.

By combining Dancik’s Labor/Expense items and Job Orders concept, the system can effectively manage the order and billing cycle for the fabrication of natural stone.

There are many strategies and accounting techniques that can be applied to fabrication. These strategies should be reviewed by your accounting department and/or outside auditors, and adjusted as needed.

Fabrication_Strategy_1 -_Direct Access to Slab Industry

Fabrication_Strategy_2_-_Fabrication_Shop_has_Separate_Inventory_in_SF_not_Slabs

Fabrication_Strategy_3_-_Use_Light_Manufacturing_System

Fabrication_Strategy_4_-_All_Material_and_Labor_Itemized

Fabrication_Strategy_5_-_One_Price_Followed_by_Job_Costs

Fabrication Strategy #1 - Direct Access to Slab Industry

This strategy assumes that you inventory your slabs in individual pieces with lengths and widths.

1. orders use the J* prefix to trigger “Job Style” invoices

2. orders begin with the F6 message lines, prefixed with J*, describing the job

3. each slab used is included on the order, and resized as needed

4. Labor/Expense items are created for each labor activity or expense, and are included on the order for job costing purposes

5. Bills of Material are set up for easy grouping of fabrication labor items

|

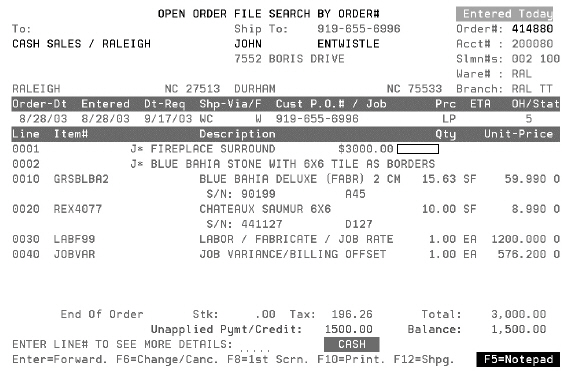

This order uses the “Job Style” which is triggered by a message line prefixed with J*. Only the J* lines print on an invoice, quotation, or order acknowledgement.

Some of the features of this order are as follows:

1. Use the J* lines to describe the job. You can optionally include the price in the comment line, but it is not needed, as the total is still calculated.

Note: You would not want to key a comment line with a price that did not agree with the actual total.

2. This job includes a slab item (1 30 x 75 slab), 10 SF of tile, and $1200.00 of labor. The salesperson quoted the job at $2000 plus tax. Because the actual inventory and labor were calculated at less than $2000, a line is added to “plug the difference”. This line adds $585.22 of pure profit margin, and makes the order equal the price quoted by the salesperson. If the salesperson underbid, you would need a negative Job Variance line.

3. This strategy preserves the ability to analyze profitability of each item, because within the order, material and labor each have their own portion of the job price.

4. The customer only sees the J* lines, and never sees the itemized prices.

Fabrication Strategy #2 - Fabrication Shop has Separate Inventory in SF, not Slabs

Steps 1, 2, 4, and 5 are the same as for strategy #1.

1. Slabs move from the regular slab inventory to the fabrication warehouse, under different item numbers. The new item numbers are set up in SF, not by individual slabs. This way various cuts and pieces do not need to be accounted for individually. Instead, a SF allocation is made for each type of stone, for each job.

2. To move slabs from the regular inventory to the fabrication warehouse, you must write them off with an adjustment code that means “deducted for use in fabrication”, and adjust them into the fabrication warehouse using that same adjustment code.

Note: If you do not wholesale slabs, then you can receive slabs as SF material (instead of individual slabs) and skip steps 3 and 6.

|

Some of the features of this order are:

This order uses the J* (Job Style) feature and the other features of strategy #1.

This order differs from the previous order in that the stone item is a regular serialized item, instead of a slab item. In a fabrication business where slabs are not wholesaled to the trade, you may not want to keep the inventory in slabs. In a fabrication shop, there are many cuts leaving many shapes and sizes, and it may be easier to just track the SF per item in stock. In this example, 15.63 SF of stone is used, but no slabs are identified.

Fabrication Strategy #3 - Use Light Manufacturing System

This strategy assumes you make a standard set of fabricated items, rather than every job being completely customized. For example, you make a standard set of countertop sizes, with standard sink cut-outs.

1. Special items are set up for the “finished goods”, such as items for 24x96 countertop, etc. These items are coded with the special policy code for “Light Manufacturing Item”. These items are assigned a price and a “standard cost”. The prices and costs may be by the PC, the SF, etc.

2. Bills of Material are set up for each Light Manufacturing Item, including all components, such as 16 SF of granite, 1 PC backerboard, etc. Labor items can be included on the Bill of Material.

3. Orders are placed using the special Light Manufacturing Items. Refer to documentation on the “Light Manufacturing System” for further details.

|

This order uses the Light Manufacturing System:

Item GRSGRAN24X120 is a light manufacturing item, with its own price, cost, and Bill of Materials. The three items below item GRSGRAN24X120 (lines 20, 30 and 40) are components of the countertop being manufactured. Components are identified by the dash next to each line number. The components have no price, and are used only for adjusting inventory.

The two additional labor items shown are special services not included in the standard countertop, and are billed and costed on their own separate lines.

This strategy combines previously released functionality (the Light Manufacturing process) with new labor/expense items.

This strategy preserves the ability to analyze the profitability at the item level as well as the job level. The components shown with no price are actually never invoiced. They automatically become inventory adjustments as part of the Light Manufacturing process.

The Light Manufacturing System is recommended when you are fabricating standard finished products. If you are fabricating custom (one of a kind) products, then the other strategies included in this section are more applicable.

Fabrication Strategy #4 - All Material and Labor Itemized

This strategy assumes that you have an established price, cost and gross profit on each item - material and labor.

1. Orders do not necessarily use the J* feature, because all items are priced and may be shown on the order and invoice.

2. Slabs, tiles, and other products are included on the order, each with its own price, cost, and gross profit.

3. Labor/Expense items are also itemized, each with its own price, cost, and gross profit.

4. This strategy works just like any other “non-job” order. The total of the “job” is simply the total of the itemized charges.

|

This order uses a pricing strategy very similar to how regular inventory orders are processed.

Each item is separately priced and costed - materials and labor/services.

The inventory item is priced as it would be sold without labor.

The labor is based on pre-defined rates for each service.

The labor has pre-defined costs that were either negotiated with third-parties, or represent an internal cost of employees to perform these functions.

This strategy preserves the ability to analyze profitability for each item as well as for the job.

In terms of being consistent with the way non-job style sales are analyzed, this strategy is best. Each item, material or labor, maintains its own profit margin statistics at every level of the system - line item level, product line level, etc. However, this strategy requires the discipline of a well thought out price list for your services and labor. You may also combine this strategy with strategy #1 and #2, by rounding up to a job price using a “Job Variance” item to “plug in the extra profit”, and then using the J* feature to hide the details from the customer.

Fabrication Strategy #5 - One Price, Followed by Job Costs

This strategy assumes that you build the price of the job into the price of the material being ordered, or into any single line item on the order.

1. Orders do not require the use if the J* feature, although the J* feature may be used if you do not want to show all of the detail lines.

2. The first line on the order is the main material priced inclusive of the fabrication. For example, perhaps a product sold for $5.99 per SF without fabrication, and sells for $18.99 per SF with fabrication. This concept also applies to products sold on an “installed” basis.

3. All other lines on the order are entered without prices, and are listed for job costing purposes. Since the labor is already built into the price of the main item, only the cost of the labor is required on these additional lines.

4. The gross profit margin on each item fluctuates from high margin on the main product, to negative margin on all of the other lines on the order. In this strategy, gross profit margin is only meaningful for the order as a whole.

Note: This is not Dancik’s recommended strategy, as it does not allow for accurate sales and profit analysis by item. Strategies 1, 2, 3, and 4 can all be used in ways that allow for accurate sales and profitability at the line and item level, as well as the job level.

|

This order puts all the price (and gross profit) into the main item being sold.

1. The J* feature is used in the example above, but it is not necessary as the services listed have no prices. The entire price is based upon the 26.50 SF of the Blue Bahia stone at $100.00 per SF.

2. The labor is itemized, but at no price, because the price of the labor is included within the $100.00 per SF of the material. Only the costs of the labor are needed.

Note: The unit price for the labor is shown as .001 EA, which when extended comes out to zero. However, by using features of the Price File, such as restriction codes, the unit price can be made to show as .000.

3. In this example, all of the profit margin is included in line 0010, the material. The labor has a cost but no price, and therefore has a negative profit margin. The costs of the labor should be actual costs, allowing for accurate profit reporting for the order. The following screen shows the same order, but using View 7 of Order Inquiry, the “GP Analysis View”.

View 7 (GP Analysis View) of Job (Strategy #5)

|

1. This view of the order shows the gross profit for each line, as well as for the entire job (order).

Note: This is View 7, the GP Analysis View, on Order Inquiry.

2. Line 0010, on its own, has a GP% of 69%. However, the labor lines have costs of $105, $475, $150, and $40 respectively, and that reduces the overall GP% of the job to 39.94%.

3. This strategy allows for accurate job-by-job and customer-by-customer analysis of profitability, but does not allow for accurate item by item profitability. In this example, it appears that your GP% is 69% for the stone, and that you lose money on all labor. If you choose to utilize this strategy, make sure you understand the affect it has on item analysis. This is not a recommended strategy for statistical analysis.